If you’ve opened your auto insurance renewal notice lately, you’ve likely experienced a moment of financial sticker shock. You’re not alone. After years of relatively stable premiums, car insurance costs in the United States have become one of the fastest-rising household expenses, leaving many drivers wondering: What is happening, and will it ever stop?

In 2026, the average American driver is projected to pay $2,256 annually for auto insurance . While the rate of increase has slowed compared to the historic jumps of recent years, premiums remain at record highs. The factors behind this surge aren’t simple—they represent a convergence of economic pressures, technological changes, legal trends, and climate risks that together are reshaping the auto insurance landscape.

The Numbers Tell a Painful Story

To understand today’s crisis, we need to look at the trajectory of recent years. From 2021 through 2023, insurers faced an unprecedented environment. Inflation spiked, supply chains fractured, and the cost of everything from replacement parts to used vehicles skyrocketed . Insurance companies responded with aggressive rate increases. The national average premium rose a staggering 18% from 2023 to 2024 alone .

The good news for consumers is that the pace of increases appears to be moderating. The typical U.S. driver saw rates rise only 3% from 2024 to 2025, and projections for 2026 suggest some states may even see modest declines . But this stabilization comes after premiums have already climbed to levels that strain household budgets. According to The Zebra Premium Pressure Index, Americans are now spending 2.6% of their annual income on auto insurance—a figure that jumps to nearly 5% in states like Arkansas, Louisiana, and Florida .

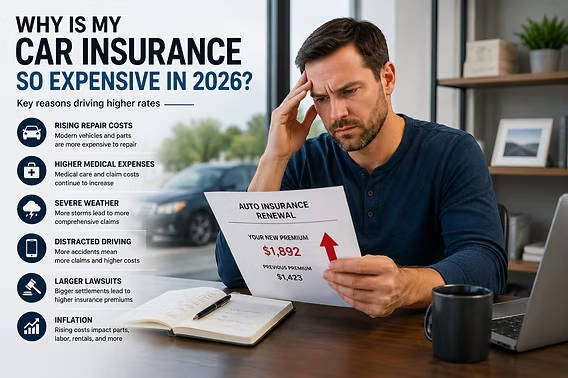

The Five Forces Driving Rates Higher

1. The Rising Cost of Everything Automotive

When your car needs repairs after an accident, the bill today is dramatically higher than it was just a few years ago. Maintenance and repair costs rose 6.1% year-over-year in May 2026, and used vehicle prices have resumed their upward climb after a brief dip . Several factors drive this:

Advanced Technology: Modern vehicles are essentially computers on wheels. Bumpers now house radar sensors, windshields integrate cameras for lane-keeping assist, and headlights use expensive LED arrays. According to AAA, advanced driver assistance systems (ADAS) can add up to 37.6% to total repair costs after a crash . What used to be a simple fender bender now requires recalibration of multiple systems.

Labor Shortages: The auto repair industry continues to struggle with a shortage of trained technicians. Fewer mechanics, combined with the increased complexity of modern vehicles, means labor rates are climbing and repairs take longer. This directly increases the cost of every claim.

Electric Vehicles: While still a relatively small portion of the nation’s 297 million vehicles, EVs are significantly more expensive to repair—roughly 29% more than their gas-powered counterparts due to specialized components, battery safety protocols, and limited repair networks .

Tariff Uncertainty: Geopolitical tensions and new tariff proposals on auto parts from China, Canada, and Mexico could create fresh supply chain disruptions. Replacement parts like windshields and airbags could become more expensive and harder to source, further driving up claims costs .

2. Legal System Abuse and Social Inflation

Insurers point to a phenomenon called “social inflation”—the rising cost of insurance claims driven by increased litigation, larger jury awards, and changing societal attitudes toward corporations. This is not just an industry talking point; the numbers are striking.

A Triple-I and Casualty Actuarial Society analysis found that excessive litigation added an estimated $281.2 billion in increased liability insurance losses from 2015 to 2024—a figure that cannot be explained by economic inflation alone . Roughly one-third of increasing inflation in auto liability losses stems from these legal trends .

Third-party litigation funding has become a “global multi-billion-dollar asset class,” according to the National Insurance Crime Bureau, with $380 million spent on online advertising alone last year to attract plaintiffs . These legal trends hit some states harder than others. In New York, for example, the average personal auto injury claim is **$46,726—more than double the national average**—and suspicious fraud reports for no-fault auto insurance have increased 80% over the last five years .

States are beginning to respond. Florida’s tort reforms have already driven substantial premium reductions and renewed private market competition in the state . New York recently passed a package of auto insurance reform bills, including a $100,000 cap on noneconomic damages for at-fault, uninsured, or impaired drivers .

3. Severe Weather and Climate Risk

Hurricanes, hailstorms, wildfires, and flooding aren’t just destroying homes—they’re also taking a massive toll on vehicles. Insured losses from natural catastrophes were on track to exceed $135 billion in 2024, and the frequency and severity of extreme weather events continues to increase .

Hurricane Helene alone caused flood damage to as many as 138,000 vehicles across six states . These catastrophic events cascade through the insurance system, driving up reinsurance costs (the insurance that insurers buy to protect themselves) and ultimately reaching consumers in the form of higher premiums .

4. Medical Cost Inflation

When an accident results in injuries, the medical costs involved have risen far faster than general inflation. Since 2000, the cost of medical care has increased by 121.3%, compared to 86.1% for consumer goods and services . Rising drug prices, advanced medical equipment, administrative overhead, and increased labor costs continue to push these expenses higher with no immediate relief in sight .

5. The Pandemic’s Lingering Aftermath

The COVID-19 pandemic created a perfect storm of disruptions that continue to affect the insurance market today . Many states froze insurers’ ability to raise rates during the pandemic, creating a “rate catch-up” effect when restrictions were lifted . Supply chain bottlenecks and microchip shortages caused new car prices to soar, which in turn pushed used car values to record highs . Higher car values mean higher claim payouts, which means higher premiums.

Distracted driving also spiked during the pandemic and remains at elevated levels. According to a recent Nationwide survey, seven in ten commercial drivers report increased distraction and reckless driving from others on the road—a 10-point increase from the previous year .

A Tale of Two Markets: Winners and Losers by State

The impact of these factors varies dramatically across the country. The Zebra’s 2026 State of Auto Insurance Report projects that 19 states will see premium increases in early 2026, while 13 states may see decreases .

States Hit Hardest:

- Oregon, Maryland, and Utah are forecast to see 8% to 21% increases .

- Six states recorded increases of more than 50% from 2024 to 2025: Louisiana, Nevada, New York, Georgia, Maryland, and Utah .

States Seeing Relief:

For residents in high-impact states, the affordability crisis is severe. In Arkansas, Louisiana, and Florida, families are spending nearly 5% of their annual income just on auto insurance .

What Insurers Are Doing (and What You Can Do)

The Industry Response

After years of underwriting losses, insurers have regained profitability. Progressive posted a combined ratio of 86.4% in the first quarter of 2026 (anything under 100% indicates underwriting profit), while Allstate reported an underlying auto combined ratio of 89.5% . Both companies have grown their policy counts as profitability improved following several years of substantial rate increases .

But this profitability may be short-lived. With inflation accelerating again—the Consumer Price Index climbed 4.2% in May 2026—insurers may need to repeat the process of raising premiums to keep pace with rising claim costs .

How to Protect Your Wallet

While you can’t control inflation or weather patterns, there are practical steps you can take to manage your auto insurance costs :

Shop Around Relentlessly: Rates can vary dramatically between insurers for the same driver. With 57% of customers actively seeking new coverage within the past year, comparison shopping has become more important than ever .

Consider Telematics: Usage-based insurance programs that monitor your driving habits can reduce premiums by 30% or more for safe drivers . Technologies that monitor mileage, braking, acceleration, and other driving patterns provide real-time feedback that can adjust unsafe behavior.

Drive Safely: It sounds obvious, but distracted driving leads to an average 17% premium increase . Put down the phone, maintain safe following distances, and avoid speeding.

Choose Your Vehicle Wisely: Among non-luxury brands, the Nissan GT-R is the most expensive to insure at nearly $400 per month**, while the Ford Bronco costs just **$76 per month . Before buying a car, research insurance costs for specific models.

Review Your Coverage: Make sure you’re not paying for coverage you don’t need. As your vehicle ages, consider dropping comprehensive and collision coverage if the car’s value no longer justifies the premium.

Looking Ahead

The trajectory of auto insurance affordability will depend on how effectively insurers adapt to heightened volatility and complexity. As KPMG analysts note, the current challenge “is not cyclical noise; it reflects structural shifts in risk, cost and consumer expectations” . Enhanced modeling, more granular risk assessment, and sustained performance discipline will shape outcomes, even as external pressures persist .

The coming period will test the industry’s ability to balance risk accuracy with accessibility, and profitability with the fundamental promise of insurance itself . For now, American drivers are left navigating a market where premiums remain high, relief is unevenly distributed, and the factors driving costs show no sign of fully reversing.